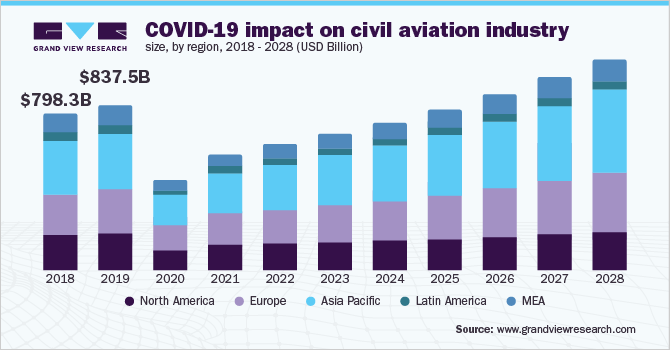

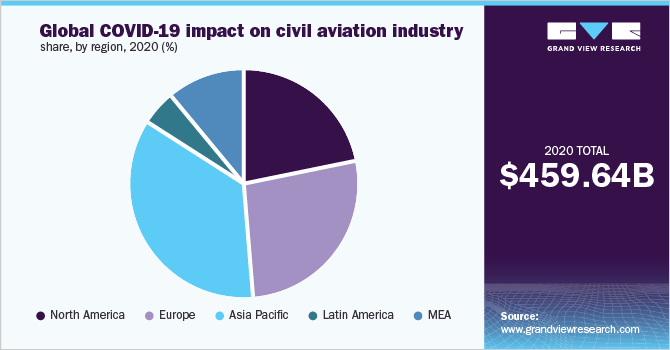

The outbreak of the COVID-19 pandemic has had a significant impact on the overall aviation industry. The civil aviation industry particularly confronted considerable revenue losses, with revenues plummeting over the year from USD 837.53 billion in 2019 to USD 459.64 billion in 2020 as travel restrictions and social distancing norms drastically reduced the demand for air travel during the first two quarters of 2020. Although the industry has been showing some signs of recovery since the third quarter, the recovery rate remains sluggish and it is anticipated that revenues would gradually attain their pre-pandemic levels only over the next five years. As such, the market is poised for a gradual recovery to generate revenues worth USD 1.09 trillion in 2028, registering a compound annual growth rate (CAGR) of 8.9% from 2021 to 2028.

Restrictions on air travel left the civil aviation industry crippled by financial crises. Prominent airline operators had to ground their fleet and temporarily halt their operations. Moreover, a significant part of the grounded fleet is estimated to never return to operations. For instance, American Airlines announced the retirement of its 767,757, E190, and A330-300 fleet in May 2020, owing to a significant drop in air passenger traffic. Gaining travelers’ confidence in the aircraft safety measures being implemented is turning out to be a new challenge for airline operators. To address this challenge, airlines are adopting various preventive measures, such as sanitizing the cabins regularly and installing advanced High-Efficiency Particulate Air (HEPA) filters inside the cabins, to ensure the safety of their passengers. However, airlines would be facing additional overhead expenses owing to these measures.

Airlines have conventionally relied on the historical database of passengers to forecast the demand and make strategic decisions on ticket pricing. However, in the wake of the outbreak of the pandemic, airlines are upgrading their data models to predict demand for specific routes. At the same time, airline operators and airport authorities are also adopting solutions based on the latest and advanced technologies, such as the Internet of Things (IoT), to provide contactless service to their passengers. The key application areas where the airlines are expected to increase the adoption of advanced technologies in the near future include baggage handling, thermal screening, contactless security for check-in and check-out, and in-flight entertainment.

Business travel has been one of the critical sources of income for the aviation industry. Continued globalization and the widening geographical outreach of companies have been particularly driving the demand for business air travel. However, the frequency of business-related personal meetings has reduced significantly due to the pandemic outbreak and the subsequent restrictions on travel and movement of people. As such, several organizations have reduced the number of in-person meetings and particularly axed down mid-level and low-level employee meetings to ensure employee safety. As per a recent survey by the Global Business Travel Associations (GBTA), 98% of the employees of multinational companies canceled their international business trips in 2020. Similarly, 92% of the employees have cut down most of their domestic business travel.

Domestic air operations are expected to recover ahead of international travel in the near future. Various governments are gradually easing travel restrictions on domestic routes as part of the efforts to boost economic growth. Having confronted heavy losses throughout 2020 due to travel bans and restrictions, airlines across the globe remain keen on reducing their operating costs and are preferring to operate short-haul and medium-haul flights. In India, especially, the revival of overseas travel is projected to be more challenging and slower than domestic travel. This will, in turn, result in heavy losses for the country’s international carriers, such as Air India, which generates approximately 60% of its revenues via international operations.

The Asia Pacific region accounted for the highest revenue share of the civil aviation industry and is expected to continue leading over the forecast period. The pandemic has taken a severe toll on the regional aviation industry, which has witnessed the highest revenue decline over the past year. Nevertheless, air passenger traffic is poised for a gradual recovery in line with the easing restrictions on domestic travel. Airline operators across the region are realigning their operational strategies to meet the fluctuating demand for air travel. Our research findings suggest that several airlines may face financial crises and government intervention and financial assistance would be essential to support their operations. India, Sri Lanka, Japan, Indonesia, Malaysia, the Philippines, and the Republic of Korea, are among the major countries in Asia Pacific where carriers are seeking financial support from their respective governments. On the other hand, the governments in Australia, Singapore, Hong Kong, and New Zealand have already extended their supportive measures for their respective airlines.

Europe is expected to exhibit a CAGR of more than 9% from 2021 to 2028. The U.K., Germany, France, Spain, and Italy are among the most prominent aviation markets across Europe, where air travel demand has been plummeting significantly owing to strict quarantine rules. Supporting the above fact, a recent passenger survey conducted by the International Air Transport Association (IATA) revealed that approximately 76% of the people in Germany, 83% in the U.K., and 78% in France remained reluctant to travel if quarantine norms are in place. Fast track vaccination is set to play a pivotal role in elevating air travel demand over the next couple of years.

Historically, airline operators in the Middle East and Africa have raked significant revenues from international routes rather than domestic operations, given the exceptionally high demand across long-haul flights, unlike the rather limited demand for short-haul flights. Emirates, Etihad, Qatar, and Oman Airways are among the key regional airline operators, which had to confront severe revenue declines in the wake of the outbreak of the pandemic. These airlines are responding to the situation by restructuring their business models to reduce their reliance on the international market, augment revenues, and recover from the losses.

Downsizing the fleet and reducing the operational costs are among the standard measures being pursued by airline operators to tackle the financial crisis. Airlines are focusing on adopting advanced technologies to improve fleet performance. They are also adopting solutions based on artificial intelligence and machine learning to analyze customer feedback and increase customer retention. The adoption of such solutions can potentially open new opportunities for the carriers to offer a personalized experience, enhance passenger service, and improve the retention rate. Moreover, key airline operators are also putting a strong emphasis on highlighting the safety measures they are pursuing. Maintaining competitive pricing amid the current critical financial situation is impending significant cost pressures on airline operators. At this juncture, airlines have adopted a flexible scheduling policy to attract and retain passengers and improve their revenue position. For instance, American Airlines has announced to eliminate change fees to give passengers more flexibility while planning to travel. The primary carriers operating across the aviation industry include legacy airlines and Low-Cost Carriers (LCCs) including:

Report Attribute

Details

Market size value in 2021